At AlbaCore, we focus on the long-term. As one of Europe’s leading alternative credit specialists, we invest in private capital solutions, opportunistic and dislocated credit, and structured products.

Discover moreInvestment strategies

Insights

formerly Realindex Investments

Leader in active quantitative equities across Australian equities, global equities, emerging markets and global small companies.

Backed by a unique blend of research, portfolio construction and risk management, focused on uncovering original insights and translating them into investment strategies that are active and systematic, aiming to generate alpha.

Discover moreInvestment strategies

Insights

- Electric Vehicles are coming, charging infrastructure is the real barrier

- EV a $US1.4 trillion opportunity for utilities as grids become more essential

- Responsible investors can accelerate EV uptake and the drive to net zero

First Sentier Investors recently presented at the Responsible Investment Association Australasia (RIAA) annual conference and hosted a design lab on how responsible investors can shape the future of Electric Vehicles (EV). This paper outlines the key challenges for EV acceptance, analyses the rollout of EV charging infrastructure around the world, and considers practical ideas for investors to super-charge the uptake of EV.

Transport is next focus for net zero

Staying on the path to net zero carbon emissions by 2050 is critical to limiting the impact of global warming. Utilities have made tremendous progress in reducing emissions from the power sector over the last decade, replacing finite energy from coal and gas with renewable energy from wind and solar. With this trend well entrenched, transport is now the largest contributor to carbon emissions in many countries.

With around 75%1 of transportation emissions coming from road vehicles, electrification of cars, trucks, vans, buses and motorcycles is the challenge and the opportunity over the next decade. Focus shifts to transport.

Energy-related CO2 emissions by sector (US) (billion metric tons)

Source: EIA Annual Energy Outlook 2022, First Sentier Investors

Electric vehicles are coming

Sales of passenger EV globally were 6.6m in 2021 up from 3.2m in 2020 and 2.1m in 2019, according to BloombergNEF (BNEF).2 The researcher estimates EV sales represented 9% of all passenger vehicle sales. Leading markets for EV sales included Germany (26%) and UK (21%).

Most governments around the world recognise the need to accelerate uptake of EV to address the climate impacts of transport. European policies have been particularly supportive with the region’s largest car manufacturer Volkswagen Group expecting electric vehicles to represent 70% of sales by 2030 and to stop selling internal combustion engines by 2035.3

EV share of passenger vehicle sales

Source: BNEF Long-Term Electric Vehicle Outlook 2022, First Sentier Investors

The scale and range of EV availability has been impacted by R&D lead times, COVID disruptions and supply chain constraints. Tesla has been leading the charge (Model 3 sold 470k units in 2021) but a new range of EV from established manufacturers will be available soon, including the best-selling vehicle in the US the Ford F-150. Momentum is building.

Audi e-tron GT

Ford F150 Lightning

Source: Audi, Ford

EV charging the real barrier

As the new range of EV hit the showroom floor, the real challenge begins. A Deloitte survey4 found that the number one barrier to EV adoption was a lack of charging infrastructure (33% of participants). If we add driving range (22%) and charging time (16%), then it could be argued more than 70% of the problem is about charging infrastructure.

Barriers to EV adoption (UK)

Source: Deloitte 2020 Global Auto Consumer Study, First Sentier Investors

For the conversion to EV to be a positive experience for consumers, the rollout of charging infrastructure has to lead vehicle sales. While more than 80% of passenger EV charging is likely to be done at home, addressing the anxiety issues above will require a significant investment in public charging.

EV sales and public charging infrastructure (global)

Source: BNEF Long-Term Electric Vehicle Outlook 2022, First Sentier Investors

The global experience to date suggests a ratio of EV to public charger at 15:15. This ratio varies widely by country and should logically correlate with population density. Countries with high density like Netherlands, South Korea, China and Italy have ratios of less than 10:1. Populations with more detached housing like Germany, US, Sweden and Australia are likely to need less public charging with ratios at more than 20:1.

As the fleet of passenger EV expands, so too will the need for EV charging. BNEF estimates this investment opportunity could represent $US1.0–1.4 trillion over the next 20 years, roughly split evenly between private, public and commercial uses.6 We believe the opportunity is big.

EV public charging infrastructure by country

Source: BNEF, First Sentier Investors as at 31 December 2021

Finding the right business model

There are a number of ways to play the EV theme. Investing in EV vehicle and battery manufacturers like TSLA, BYD or CATL. Gaining exposure to key minerals like lithium, cobalt or nickel. However, manufacturers are likely to face significant competition over time while commodities could be a wild ride. In this report we focus directly on EV charging infrastructure.

A number of EV charging infrastructure companies listed in recent years – ChargePoint, EVgo, Allego, Wallbox, Blink Charging and Volta. The business models vary but may include the manufacture and sale of charging hardware, installation and maintenance of the hardware, a margin on electricity sales, and software for subscription-based access to charging networks.

Initial excitement in the massive growth opportunity has been overwhelmed by the reality of heavy losses. Our analysis indicates that the business models deliver low gross margins, there are few barriers to entry, supply chain issues have delayed rollouts and the “land-grab” for charging sites is expensive. The financials of ChargePoint highlight the significant (mis) allocation of capital to research and development, sales and marketing, and general and administrative expenses.

ChargePoint operating loss waterfall ($m)

Source: ChargePoint, First Sentier Investors. Year ended 31 January 2022

Stock price performance of the charging infrastructure companies has been dismal and investor capital would have been better invested in a regulated utility.

EV charging stock performance ($/share)

Source: Bloomberg, First Sentier Investors as at 31 May 2022

In our view, regulated utilities with electricity distribution networks represent a more compelling exposure to EV charging infrastructure. With the right policy and regulatory settings in place, utilities are well placed to deliver a coordinated rollout of a consistent product at a reasonable cost. By including the EV charging infrastructure rollout costs in the regulated rate base, along with the required distribution and transmission network upgrades, costs can be shared across the customer base. We believe utilities are the best play.

Xcel Energy provides a useful case study. Xcel owns electricity distribution networks in Minnesota, Colorado, Wisconsin and New Mexico with approved EV programs. The utilities intend to invest over $US2 billion over the next 10 years to enable 1.5m EV in their service territories. In current dollars that equates to around $US700 for charger equipment plus $US700 for installation for each customer.

Xcel Energy EV Infrastructure Plan

Source: Xcel Energy, First Sentier Investors

Residential

- Charger installs and services

- Rebates for vehicles and charger installs (rate based)

Commercial

- Charging equipment/installs for cities, schools and businesses

- EV purchase rebates (rate based)

Public

- Stations in major corridors and underserved communities

This capital investment will add to rate base growth, which in turn will add to earnings growth. Xcel is targeting 5–7% EPS growth which should be sustainable over the long-term.

Xcel is not alone. Across the US there are now 60 electric companies in 35 states or territories with regulatory approvals for EV programs7, including PG&E/Edison/Sempra in the west, ConEd/PSEG/Avangrid/Eversource in the north-east and Duke/NextEra in the south-east.

The investment opportunity could be materially higher if customers demand faster charging. While a home AC installation for overnight charging should price below $2,000, a fast DC charger that gets you back on the road in 20 minutes could cost more than $US100,000.

Type and cost of EV charging infrastructure

Hardware and installation cost assumptions in 2020 (US $)

Source: Electric Vehicle Council, BNEF, First Sentier Investors

EV charging will have secondary effects on utilities. EV will likely represent 10–20% of electricity load over the coming decades. Ten years ago there were fears that conservation/efficiency measures and distributed generation would render the grid redundant. Now the opposite is true, with electrification of transport and heating, datacentres and even bitcoin mining creating strong growth in volumes. The grid looks set to become even more essential.

Customers may also want to ensure that the electricity for EV charging is from renewable sources. We believe this will lead to additional investment in solar and wind generation and associated transmission lines.

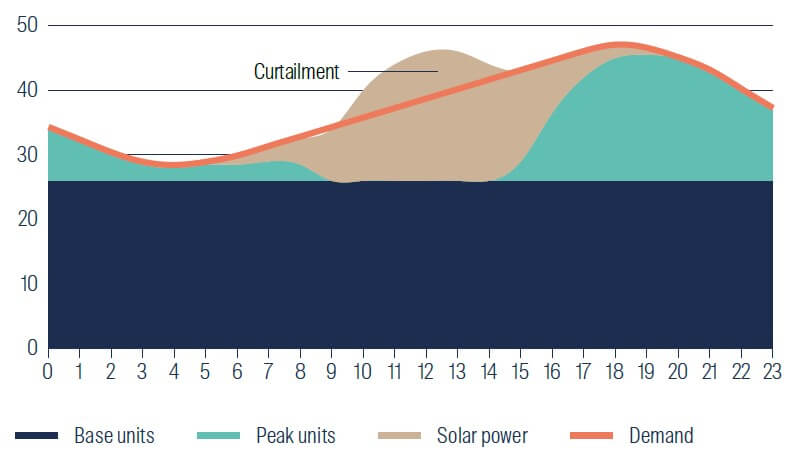

EV charging may also stimulate demand for smart grid solutions. A growing challenge for electricity grids is that renewable supply peaks during the middle of the day, whereas demand peaks in the evening. Significant development of solar capacity has resulted in summer days where power supply is well in excess of demand. Grids are forced to reject or curtail solar energy to maintain balance in the system.

Electricity demand/supply by time of day (TWh)

Source: First Sentier Investors. Simplified model

Most EV spend 80–90% of the time parked. Vehicle-to-grid (V2G) bi-directional charging could allow the EV fleet to act as a network of batteries, charging from the grid during the solar peak and releasing to the grid in the demand peak. V2G charging could (1) reduce renewable energy curtailment, (2) help grid operators manage peak demand and (3) offer a peak/off-peak price arbitrage. International Renewable Energy Agency (IRENA) estimates that V2G charging could reduce peak load by 4% and energy costs by 13%.

We believe EV charging is an enormous investment opportunity with numerous challenges. So how can Responsible Investors contribute to accelerating the uptake of EV? Below are a few ideas worth considering:

- Allocate investor capital towards electric utilities which have regulatory approval to rollout EV charging infrastructure

- Lobby energy regulators to include EV charging infrastructure plus associated electricity distribution and transmission network upgrades in the rate base to encourage investment. Multi stakeholder engagement with utilities, regulators and industry bodies could be a useful tool

- Real estate investors require minimum 1-in-5 vehicle parking spaces to be EV ready for new or re-developed office, commercial, housing projects

- Explore opportunities for toll road companies to develop EV fast charging and recreation areas on vacant land along suburban or intercity roads

- Challenge integrated oil companies to transform retail fuel sites into EV fast charging centres

- Allocate higher risk capital to supply chain solutions including rare metals mining, semi-conductors and battery manufacturing. Allocate capital to the manufacture of component parts such as semiconductors

- Allocate your personal capital to an EV

1 Source: International Energy Agency as at 31 December 2021.

2 Source: BloombergNEF Long-Term Electric Vehicle Outlook 2022.

3 Source: Volkswagen, May and June 2021.

4 Deloitte 2020 Global Auto Consumer Study.

5 Source: BloombergNEF Long-Term Electric Vehicle Outlook 2022.

6 Source: BloombergNEF Long-Term Electric Vehicle Outlook 2022.

7 Source: First Sentier Investors as at 31 May 2022.

Reference to the names of each company mentioned in this communication are for illustrative purposes only and are merely used for explaining the investment strategy. Any fund or stock mentioned in this presentation does not constitute any offer or inducement to enter into any investment activity nor is it a recommendation to purchase or sell any security.

Curious about what lies ahead?

Find out more about how we are shaping the future.

Important Information

This material is for general information purposes only. It does not constitute investment or financial advice and does not take into account any specific investment objectives, financial situation or needs. This is not an offer to provide asset management services, is not a recommendation or an offer or solicitation to buy, hold or sell any security or to execute any agreement for portfolio management or investment advisory services and this material has not been prepared in connection with any such offer. Before making any investment decision you should consider, with the assistance of a financial advisor, your individual investment needs, objectives and financial situation.

We have taken reasonable care to ensure that this material is accurate, current, and complete and fit for its intended purpose and audience as at the date of publication. No assurance is given or liability accepted regarding the accuracy, validity or completeness of this material and we do not undertake to update it in future if circumstances change.

To the extent this material contains any expression of opinion or forward-looking statements, such opinions and statements are based on assumptions, matters and sources believed to be true and reliable at the time of publication only. This material reflects the views of the individual writers only. Those views may change, may not prove to be valid and may not reflect the views of everyone at First Sentier Investors.

About First Sentier Investors

References to ‘we’, ‘us’ or ‘our’ are references to First Sentier Investors, a global asset management business which is ultimately owned by Mitsubishi UFJ Financial Group. Certain of our investment teams operate under the trading names FSSA Investment Managers, Stewart Investors and Realindex Investments, all of which are part of the First Sentier Investors group.

We communicate and conduct business through different legal entities in different locations. This material is communicated in:

- Hong Kong by First Sentier Investors (Hong Kong) Limited and has not been reviewed by the Securities & Futures Commission in Hong Kong. First Sentier Investors is a business name of First Sentier Investors (Hong Kong) Limited.

- Singapore by First Sentier Investors (Singapore) (reg company no. 196900420D) and this publication or advertisement has not been reviewed by the Monetary Authority of Singapore. First Sentier Investors (registration number 53236800B) is a business division of First Sentier Investors (Singapore).

- Japan by First Sentier Investors (Japan) Limited, authorised and regulated by the Financial Service Agency (Director of Kanto Local Finance Bureau (Registered Financial Institutions) No.2611)

To the extent permitted by law, MUFG and its subsidiaries are not liable for any loss or damage as a result of reliance on any statement or information contained in this document. Neither MUFG nor any of its subsidiaries guarantee the performance of any investment products referred to in this document or the repayment of capital. Any investments referred to are not deposits or other liabilities of MUFG or its subsidiaries, and are subject to investment risk, including loss of income and capital invested.

© First Sentier Investors Group

Discover more

|  |

|---|